As filed with the Securities and Exchange Commission on January 24, 2018

Registration No. 333- 222123

UNITED

STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

AMENDMENT NO. 1 TO

FORM S-4

REGISTRATION

STATEMENT

UNDER THE SECURITIES ACT OF 1933

MARATHON

PATENT GROUP, INC.

(Exact name of registrant as specified in its charter)

| Nevada | 6794 | 01-0949984 | ||

| (State

or other jurisdiction of incorporation or organization) |

(Primary

Standard Industrial Classification Code Number) |

(I.R.S.

Employer Identification Number) |

11601 Wilshire Blvd., Ste. 500

Los Angeles, California 90025

(703) 232-1701

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Merrick Okamoto, Chairman of the Board

11601 Wilshire Blvd., Ste. 500

Los Angeles, California 90025

(703) 232-1701

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Harvey J. Kesner, Esq.

Arthur S. Marcus, Esq.

Sichenzia Ross Ference Kesner LLP

1185 Avenue of the Americas, Suite 3700

New York, New York 10036

(212) 930-9700

Approximate date of commencement of proposed sale of the securities to the public: As soon as practicable after the effective date of this registration statement.

If the securities being registered on this form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box. [ ]

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. [ ]

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | [ ] | Accelerated filer | [ ] | |||

| Non-accelerated filer | [ ] (Do not check if a smaller reporting company) | Smaller reporting company | [X] | |||

| Emerging growth company | [ ] |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. [ ]

If applicable, place an X in the box to designate the appropriate rule provision relied upon in conducting this transaction:

Exchange Act Rule 14e-4(i) (Cross-Border Tender Offer) [ ]

Exchange Act Rule 14d-1(d) (Cross-Border Third-Party Tender Offer) [ ]

CALCULATION OF REGISTRATION FEE

| Title of Each Class of Securities to be Registered | Amount to be Registered | Proposed Maximum Offering Price Per Security | Proposed Maximum Aggregate Offering Price | Amount of Registration Fee | ||||||||||||

| Common stock, par value $0.0001 per share | 4,372,429 | (1) | $ | 5.62 | (2) | $ | 24,573,050.98 | (2) | $ | 3,059.34 | ||||||

| Common stock, par value $0.0001 per share, underlying Series C Preferred Stock | 122,302,128 | (1) | $ | 5.62 | (2) | $ | 687,337,959.36 | (2) | $ | 85,573.58 | ||||||

| Common stock, par value $0.0001 per share, underlying Series E Preferred Stock | 5,511,702 | $ | 5.62 | (2) | $ | 30,975,765.24 | (2) | $ | 3,856.48 | |||||||

| Common stock, par value $0.0001 per share, underlying Series E-1Preferred Stock | 5,067,435 | (1) | $ | 5.62 | (2) | $ | 28,478,984.70 | (2) | $ | 3,545.63 | ||||||

| Total | 137,253,694 | $ | 5.62 | $ | 771,365,760.28 | $ | 96,035.03 | |||||||||

| (1) | Reflects the number of shares of the registrant to be issued to the security holders of Global Bit Ventures, Inc. (“GBV”). | |

| (2) | Pursuant to Rule 457(c) under the Securities Act and solely for the purpose of calculating the registration fee, the proposed maximum aggregate offering price is equal to the product obtained by multiplying (a) $5.62, which represents the average of the high and low prices of the registrant on December 14, 2017, by (b) the number of shares of registrant’s securities issuable in connection with the Merger. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this proxy statement/prospectus/information statement is not complete and may be changed. Marathon Patent Group, Inc., may not sell these securities pursuant to the proposed transactions until the Registration Statement filed with the Securities and Exchange Commission is effective. This proxy statement/prospectus/information statement is not an offer to sell these securities and is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to completion, dated January 24, 2018

|

|

PROPOSED MERGER

YOUR VOTE IS VERY IMPORTANT

To the Shareholders of Marathon Patent Group, Inc. and Global Bit Ventures, Inc.:

Marathon Patent Group, Inc. (“Marathon”) and Global Bit Ventures, Inc. (“GBV”) have entered into an Agreement and Plan of Merger (the “Merger Agreement”) pursuant to which a wholly owned subsidiary of Marathon will merge with and into GBV , with GBV surviving as a wholly owned subsidiary of Marathon (the “Merger”). GBV and Marathon believe that the Merger will result in a combined organization with a novel business consisting of digital asset/ cryptocurrency mining.

At the Effective Time ( as defined in the Merger Agreement filed as an exhibit to Marathon’s Current Report on Form 8-K filed with the Securities and Exchange Commission on November 2, 2017 ) of the Merger, each share of (A) common stock of GBV, par value $0.0001 per share (“GBV Common Stock”) will automatically be cancelled and converted into shares of either (x) Series C Preferred Stock of Marathon (the “Series C Preferred Stock”) or (y) common stock, par value $0.0001 per share of Marathon (“Common Stock”): (B) Series A Preferred Stock, par value 0.0001 per share, of GBV (“GBV Series A Stock”) will automatically be cancelled and converted into shares of either (x) Series C Preferred Stock or (y) Common Stock; and (C) all of GBV’s outstanding convertible debt (“GBV Notes”) will automatically be cancelled and converted into shares of either (x) Series C Preferred Stock or (y) Common Stock. Marathon will not assume outstanding and unexercised warrants and options to purchase shares of GBV capital stock, and none are outstanding. The total number of shares of Common Stock and shares of Common Stock issuable under the Series C Preferred Stock is 126,674,557.

Marathon’s shareholders will continue to own and hold their existing shares of Common Stock and Marathon’s preferred stock. Marathon debt holders owning $2,613,948 of 5% convertible promissory notes (the “Marathon Notes”) as of January 22, 2018, will convert their unconverted notes into Series E-1 Convertible Preferred Stock of Marathon (“Series E-1 Preferred Stock”) if not converted prior to the closing of the Merger. Marathon Series E Convertible Preferred Stock (“Series E Preferred Stock”) holders owning 5,511.70 shares of Series E Preferred Stock convertible into 5,511,702 shares of Common Stock, as of January 22, 2018 will continue to remain outstanding. The vesting of 448,775 unexercised options to purchase shares of Common Stock, which are substantially vested, will remain outstanding as of the closing of the Merger. All 794,717 warrants to purchase shares of Common Stock are currently exercisable into 794,717 shares of Common Stock. The Common Stock, preferred stock, warrants and options will remain in effect pursuant to their terms.

Immediately after the conversion of the GBV Common Stock, the GBV Series A Stock and the GBV Notes, Marathon shall have issued 81% of its issued and outstanding Common Stock, on a fully-diluted basis, under the Merger Agreement to GBV, prior to giving effect of the (1) issuance of one million shares of Marathon’s Common Stock on December 11, 2017 at $5.00 per share in a registered offering and (2) issuance of 1,354,546 shares of Marathon’s Common Stock on December 18, 2017 at $5.50 per share in a registered offering subsequent to the Merger Agreement and other changes in Marathon’s capitalization following the date of the Merger Agreement. For these purposes, Marathon’s fully-diluted Common Stock is defined as the outstanding common stock of Marathon, plus conversion of preferred stock, options and warrants of Marathon, prior to the registered offering (the “Fully-Diluted Common Stock of Marathon”), with Marathon current shareholders, the holders of the Marathon Notes, option holders and warrant holders owning, or holding rights to acquire, approximately 19% of the Fully-Diluted Common Stock of Marathon upon closing of the Merger (as such percentages are increased or reduced for the registered offering and any other shares issued or cancelled prior to the closing of the Merger).

Marathon’s shares of Common Stock are currently listed for trading on The NASDAQ Capital Market (“NASDAQ”) under the symbol “MARA.” Prior to consummation of the Merger, Marathon intends to file an initial listing application with NASDAQ. After completion of the Merger, Marathon will be renamed “Marathon Blockchain, Inc.” (or similar) and expects to trade on NASDAQ under the symbol “MARA.” On January XX, 2018 , the last trading day before the date of this proxy statement/prospectus/information statement, the closing sale price of MARA Common Stock on NASDAQ was $x.xx per share.

Marathon is holding a special meeting of shareholders (the “Special Meeting”) in order to obtain the shareholder approvals necessary to complete the Merger and related matters. At the Special Meeting, which will be held at x:xx A.M., Eastern time, on __________[●], 2018 at the offices of Sichenzia Ross Ference Kesner, LLP, 1185 Avenue of the Americas, Suite 3700, New York, NY 10036 unless postponed or adjourned to a later date, Marathon will ask its shareholders to, among other things, approve the Merger Agreement and thereby approve the transactions contemplated thereby, including the Merger and the issuance of Marathon’s Series C Preferred Stock and Common Stock to GBV’s shareholders and an amendment to Marathon’s amended and restated articles of incorporation changing the Marathon corporate name to “Marathon Blockchain, Inc.” (or similar name), each as described in the accompanying proxy statement/prospectus/information statement.

As described in the accompanying proxy statement/prospectus/information statement, certain of Marathon’s shareholders who in the aggregate own or control the right to vote outstanding voting shares of Common Stock equal to approximately 5.9% of the outstanding shares of Common Stock are parties to agreements with Marathon, whereby such shareholders have agreed to vote their shares in favor of the adoption or approval, as applicable, of the Merger Agreement and the approval of the transactions contemplated therein, including the Merger and the issuance of shares of Marathon’s Series C Preferred Stock and Common Stock to GBV’s shareholders pursuant to the Merger Agreement.

In addition, following effectiveness of the registration statement on Form S-4, of which this proxy statement/prospectus/information statement is a part, by the Securities and Exchange Commission (the “SEC”) and pursuant to the conditions of the Merger Agreement, shareholders of GBV will each receive an action by written consent of GBV’s shareholders, referred to as the written consent, adopting the Merger Agreement, thereby approving the transactions contemplated therein, including the Merger. Therefore, holders of a sufficient number of shares of GBV’s capital stock required to adopt the Merger Agreement will be required to adopt the Merger Agreement, and no meeting of GBV shareholders to adopt the Merger Agreement and approve the Merger and related transactions will be held. Nevertheless, all of GBV’s shareholders will have the opportunity to elect to adopt the Merger Agreement, thereby approving the Merger and related transactions, by signing and returning to GBV a written consent.

As a condition to the closing of the Merger, holders of unconverted Marathon Notes will also be required to agree to convert their notes into Series E-1 Preferred Stock of Marathon. Therefore, the holders of a sufficient number of Marathon Notes will be required to provide conversion notices to Marathon.

After careful consideration, each of Marathon and GBV’s boards of directors have (i) determined that the transactions contemplated by the Merger Agreement are fair to, advisable and in the best interests of Marathon or GBV, as applicable, and their respective shareholders, (ii) approved and declared advisable the Merger Agreement and the transactions contemplated therein and (iii) determined to recommend, upon the terms and subject to the conditions set forth in the Merger Agreement, that its shareholders vote to adopt or approve, as applicable, the Merger Agreement and, therefore, approve the transactions contemplated therein. Marathon’s board of directors recommends that Marathon shareholders vote “FOR” the proposals described in the accompanying proxy statement/prospectus/information statement and that Marathon’s Note Holders sign and return the written conversion notice converting the Marathon Notes into Series E-1 Preferred Stock, and GBV’s board of directors recommends that GBV’s shareholders sign and return the written consent indicating their approval of the Merger and adoption of the Merger Agreement and the transactions contemplated therein.

More information about Marathon, GBV and the proposed transaction is contained in this proxy statement/prospectus/information statement. Marathon and GBV urge you to read the accompanying proxy statement/prospectus/information statement carefully and in its entirety. IN PARTICULAR, YOU SHOULD CAREFULLY CONSIDER THE MATTERS DISCUSSED UNDER “RISK FACTORS” BEGINNING ON PAGE 25.

Marathon and GBV are excited about the opportunities the Merger brings to both Marathon’s and GBV’s shareholders, and thank you for your consideration and continued support.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this proxy statement/prospectus/information statement. Any representation to the contrary is a criminal offense.

The accompanying proxy statement/prospectus/information statement is dated January XX, 2018 , and is first being mailed to Marathon and GBV’s shareholders on or about [●], 2018.

| By Order of the Board of Directors: | |

| /s/ Merrick D . Okamoto | |

| Merrick D . Okamoto, | |

| Chairman of the Board of Directors |

Marathon Patent Group, Inc.

11601 Wilshire Blvd., Ste. 500

Los Angeles, CA 90025

(703) 232-1701

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS

TO BE HELD ON —— , 2018

Dear Shareholders of Marathon Patent Group, Inc.:

On behalf of the board of directors of Marathon Patent Group, Inc., a Nevada corporation (“Marathon”), we are pleased to deliver this proxy statement for the proposed merger between Marathon and Global Bit Ventures, Inc., a Nevada corporation (“GBV”), pursuant to which Global Bit Acquisition Corp., a Nevada corporation and a wholly owned subsidiary of Marathon (“Merger Sub”), will merge with and into GBV, with GBV surviving as a wholly owned subsidiary of Marathon. The special meeting of shareholders of Marathon (the “Special Meeting”) will be held on ________ __, 2018 at ___ A.M., Eastern time, at the offices of Sichenzia Ross Ference Kesner, LLP, 1185 Avenue of the Americas, Suite 3700, New York, NY 10036 for the following purposes:

1. To consider and vote upon a proposal to approve the Agreement and Plan of Merger, dated as of November 1, 2017, by and among Marathon, Merger Sub, and GBV, a copy of which is attached as Annex A to this proxy statement, and the transactions contemplated thereby, including the Merger and the issuance of shares of Marathon’s Series C Preferred Stock and Common Stock to GBV’s Common Stock holders, GBV’s Series A Stock holders and GBV’s Note holders pursuant to the terms of the Merger Agreement.

2. To approve an amendment to the Amended and Restated Articles of Incorporation of Marathon to change the corporate name to Marathon Blockchain, Inc. from Marathon Patent Group, Inc. in the form attached as Annex D to this proxy statement or such other similar name as shall be chosen by Marathon.

3. To consider and vote upon an adjournment of the Special Meeting, if necessary, to solicit additional proxies if there are not sufficient votes in favor of either Proposal No. 1 or 2.

4. To transact such other business as may properly come before the Special Meeting or any adjournment or postponement thereof.

Marathon’s board of directors has fixed ______ ___, 2018, as the record date for the determination of shareholders entitled to notice of, and to vote at, the Special Meeting and any adjournment or postponement thereof. Only holders of record of shares of Common Stock at the close of business on the record date are entitled to notice of, and to vote at, the Special Meeting. At the close of business on the record date, Marathon had ____________ shares of Common Stock outstanding and entitled to vote, plus ____ shares of preferred stock outstanding and entitled to vote at the Special Meeting. Each holder of preferred stock is entitled to vote such preferred stock on an “as-converted” basis up to certain “beneficial ownership” percentage limitations equal to either 2.49%, 4.99% or 9.99% of the fully-diluted Common Stock of Marathon.

Your vote is important. The affirmative vote of the holders of a majority of the shares of Common Stock having voting power present in person or represented by proxy at the Special Meeting is required for approval of Proposal Nos. 1 and 3. The affirmative vote of the holders of a majority of shares of Marathon’s Common Stock having voting power outstanding on the record date for the Special Meeting is required for approval of Proposal No. 2.

Even if you plan to attend the Special Meeting in person, Marathon requests that you sign and return the enclosed proxy to ensure that your shares will be represented at the Special Meeting if you are unable to attend.

| By Order of Marathon Board of Directors, | |

| Merrick

Okamoto Chairman of the Board of Directors Los Angeles, California January [●], 2018 |

MARATHON’S BOARD OF DIRECTORS HAS DETERMINED AND BELIEVES THAT EACH OF THE PROPOSALS OUTLINED ABOVE IS ADVISABLE TO, AND IN THE BEST INTERESTS OF, MARATHON AND ITS SHAREHOLDERS AND HAS APPROVED EACH SUCH PROPOSAL. MARATHON’S BOARD OF DIRECTORS RECOMMENDS THAT MARATHON’S SHAREHOLDERS VOTE “FOR” EACH SUCH PROPOSAL.

QUESTIONS AND ANSWERS ABOUT THE MERGER

The following section provides answers to frequently asked questions about the Merger. This section, however, provides only summary information. For a more complete response to these questions and for additional information, please refer to the cross-referenced sections.

| Q: | What is the Merger? |

| A: | Marathon Patent Group, Inc. (“Marathon”) and Global Bit Ventures, Inc. (“GBV”) have entered into an Agreement and Plan of Merger, dated as of November 1, 2017 (the “Merger Agreement”). The Merger Agreement contains the terms and conditions of the proposed business combination of Marathon and GBV. Under the Merger Agreement, Global Bit Acquisition Corp., a wholly owned subsidiary of Marathon (“Merger Sub”), will merge with and into GBV, with GBV surviving as a wholly owned subsidiary of Marathon. (the “Merger”). |

At the Effective Time of the Merger, each share of (A) common stock of GBV, par value $0.0001 per share (“GBV Common Stock”) will automatically be cancelled and converted into shares of either (x) Series C Preferred Stock of Marathon (the “Series C Preferred Stock”) or (y) common stock, par value $0.0001 per share of Marathon (“Common Stock”): (B) Series A Preferred Stock, par value $0.0001 per share, of GBV (“GBV Series A Stock”) will automatically be cancelled and converted into shares of either Series C Preferred Stock or Common Stock; and (C) all of GBV’s outstanding convertible debt (“GBV Notes”) will automatically be cancelled and converted into shares of either Series C Preferred Stock or Common Stock. Marathon will not assume outstanding and unexercised warrants and options to purchase shares of GBV’s capital stock, and none are outstanding. The total number of shares of Common Stock and shares of Common Stock issuable under the Series C Preferred Stock is 126,674,557. After the completion of the Merger, Marathon will change its corporate name to “Marathon Blockchain, Inc.” or similar name determined by the board of directors of Marathon as required by the Merger Agreement (the “Marathon Name Change”).

| Q: | What will happen to Marathon if, for any reason, the Merger does not close? |

| A: | If, for any reason, the Merger does not close, Marathon’s board of directors may elect to, among other things, attempt to complete another strategic transaction like the Merger, attempt to sell or otherwise dispose of the various assets of Marathon, resume its patent licensing and enforcement activities and continue to operate the business of Marathon or dissolve and liquidate its assets. If Marathon decides to dissolve and liquidate its assets, Marathon would be required to pay all of its debts and contractual obligations, and to set aside certain reserves for potential future claims. There can be no assurances as to the amount or timing of available cash left to distribute to shareholders after paying the debts and other obligations of Marathon and setting aside funds for reserves. |

If Marathon were to continue its business, it would need to hire personnel necessary to resume patent licensing and enforcement activities or another business. In addition, as of January 22, 2018, Marathon’s workforce was comprised of three employees, all of whom are involved in either financial and executive roles or in conducting limited activities related to maintenance of Marathon’s patent portfolio. Marathon has ceased all new patent monetization efforts, and is expending minimal efforts maintaining and pursuing ongoing litigation and licenses. If Marathon decides to reestablish a viable operating business and/or pursue development of other businesses, Marathon will need to rebuild its senior management team and hire managerial and other personnel to lead and staff all of its necessary functions, and raise substantial funds to support these activities.

| 1 |

| Q: | Why are the two companies proposing to merge? |

| A: | Marathon and GBV believe that the Merger will result in a specialty company dedicated to pursuing blockchain and digital asset mining focused on supporting the blockchain and digital asset ecosystems. For a discussion of Marathon’s and GBV’s reasons for the Merger, please see the section entitled “The Merger—Marathon Reasons for the Merger” and “The Merger—GBV Reasons for the Merger” in this proxy statement/prospectus/information statement. |

| Q: | Why am I receiving this proxy statement/prospectus/information statement? |

| A: | You are receiving this proxy statement/prospectus/information statement because you have been identified as a shareholder of Marathon or of GBV or hold the Marathon Notes as of the applicable record date. If you are a shareholder of Marathon, you are entitled to vote at Marathon’s Special Meeting to approve the Merger Agreement and the transactions contemplated thereby, including the Merger and the issuance of shares of Marathon’s Common Stock pursuant to the Merger Agreement. If you are a shareholder of GBV, you are entitled to sign and return the GBV written consent to adopt the Merger Agreement and approve the transactions contemplated thereby, including the Merger. If you are a holder of the Marathon Notes, you are entitled to sign and return the written note conversion notice. This document serves as: |

| ● | a proxy statement of Marathon used to solicit proxies for the Special Meeting; |

| ● | a prospectus of Marathon used to offer shares of Marathon’s Common Stock in exchange for shares of GBV’s capital stock and GBV Notes in the Merger, and prospectus of Marathon to offer shares of Marathon’s Common Stock upon conversion of Series E Preferred Stock, Series C Preferred Stock and Series E-1 Preferred Stock of Marathon issued in connection with the Merger, as applicable; and |

| ● | an information statement of GBV used to solicit the written consent of its shareholders for the adoption of the Merger Agreement and the approval of the Merger and for solicitation of conversion of the Marathon Notes, as applicable, and related transactions. |

| Q: | What is required to consummate the Merger? |

| A: | To consummate the Merger, Marathon’s shareholders must approve the issuance of Marathon’s Series C Preferred Stock and Common Stock pursuant to the Merger Agreement, and GBV’s shareholders must adopt the Merger Agreement and, thereby, approve the Merger and the other transactions contemplated therein. Marathon Note holders must also convert their Notes. |

The approval of the Merger and the issuance of Marathon’s Series C Preferred Stock and Common Stock pursuant to the Merger Agreement by Marathon’s shareholders requires the affirmative vote of the holders of a majority of the shares of Marathon’s Common Stock having voting power present in person or represented by proxy at the Special Meeting. The approval of the amendments to the amended and restated certificate of incorporation of Marathon to effect the Marathon Name Change requires the affirmative vote of the holders of a majority of the shares of Marathon’s outstanding Common Stock having voting power outstanding on the record date for the Special Meeting.

In addition to the requirement of obtaining the shareholder approvals described above and appropriate regulatory approvals, each of the other closing conditions set forth in the Merger Agreement must be satisfied or waived. For a more complete description of the closing conditions under the Merger Agreement, we urge you to read the section entitled “The Merger Agreement—Conditions to the Completion of the Merger” in this proxy statement/prospectus/information statement.

| Q: | What will GBV’s shareholders, warrant holders and option holders receive in the Merger? |

| A: | As a result of the Merger, GBV’s shareholders, warrant holders and option holders will become entitled to receive shares, or rights to acquire shares, of Marathon’s Common Stock equal to, in the aggregate, approximately 81% of the Fully-Diluted Common Stock of Marathon prior to giving effect of the (1) issuance of 1 million shares of Marathon’s Common Stock on December 11, 2017 at $5.00 per share in a registered offering and (2) issuance of 1,354,546 shares of Marathon’s Common Stock on December 18, 2017 at $5.50 per share in a registered offering subsequent to the Merger Agreement with Marathon current shareholders and other changes in Marathon’s capitalization following the date of the Merger Agreement, the holders of the Marathon Notes, option holders and warrant holders owning, or holding rights to acquire, approximately 19% of the Fully-Diluted Common Stock of Marathon upon closing of the Merger (as such percentages are reduced or increased for the registered offering and any other shares issued or cancelled prior to the closing of the Merger). |

| 2 |

For a more complete description of what GBV’s shareholders, note holders, warrant holders and option holders will receive in the Merger, please see the sections entitled and “The Merger Agreement—Merger Consideration” in this proxy statement/prospectus/information statement.

| Q: | Who will be the directors of Marathon following the Merger? |

| A: | In connection with the Merger, Marathon’s board of directors will consist of those persons to be designated, pursuant to the Merger Agreement, by agreement of Marathon and GBV. As of the date hereof the following persons are contemplated to be agreed by the parties to the Merger Agreement. It is anticipated that, following the closing of the Merger, Marathon’s board of directors will be constituted as follows: |

Name |

Current Principal Affiliation | |

| Merrick Okamoto | Chairman of the Board of Directors | |

Charles Allen Edward Kovalik David Lieberman Christopher Robichaud |

GBV; BTCS, Inc. Marathon Marathon Marathon |

| Q: | Who will be the executive officers of Marathon immediately following the Merger? |

| A: | Immediately following the consummation of the Merger, the executive management team of Marathon is expected to be composed solely of members of the GBV executive management team prior to the Merger: |

Name |

Title | |

Merrick Okamoto Charles Allen |

Interim Chief Executive Officer * Chief Executive Officer | |

Michal Handerhan Francis Knuettel II |

President Chief Financial Officer | |

| * Through closing of the Merger. |

| Q: | As a stockholder of Marathon, how does Marathon’s board of directors recommend that I vote? |

| A: | After careful consideration, Marathon’s board of directors recommends that Marathon’s shareholders vote: |

| ● | “FOR” Proposal No. 1 to approve the Merger Agreement and the transactions contemplated thereby, including the Merger and the issuance of shares of Marathon’s Series C Preferred Stock and Common Stock to GBV’s shareholders and note holders in the Merger; |

| ● | “FOR” Proposal No. 2 to approve an amendment to the Amended and Restated Articles of Incorporation of Marathon to effect the Marathon Name Change; and |

| ● | “FOR” Proposal No. 3 to adjourn the Special Meeting, if necessary, to solicit additional proxies if there are not sufficient votes in favor of Proposal Nos. 1 or 2. |

| Q: | As a stockholder of GBV, how does GBV’s board of directors recommend that I vote? |

| A: | After careful consideration, GBV’s board of directors recommends that GBV’s shareholders execute the written consent indicating their vote in favor of the adoption of the Merger Agreement and the approval of the Merger and the transactions contemplated by the Merger Agreement. |

| 3 |

| Q: | What risks should I consider in deciding whether to vote in favor of the Merger or to execute and return the written consent, as applicable? |

| A: | You should carefully review the section of this proxy statement/prospectus/information statement entitled “Risk Factors,” which sets forth certain risks and uncertainties related to the Merger, risks and uncertainties to which the combined organization’s business will be subject, and risks and uncertainties to which each of Marathon and GBV, as an independent company, is subject. |

| Q: | When do you expect the Merger to be consummated? |

| A: | We anticipate that the Merger will occur sometime soon after the Special Meeting to be held on ____________ __, 2018 but we cannot predict the exact timing. |

| Q: | What do I need to do now? |

| A: | Marathon and GBV urge you to read this proxy statement/prospectus/information statement carefully, including its annexes, and to consider how the Merger affects you. |

If you are a shareholder of Marathon, you may provide your proxy instructions in one of two different ways. First, you can mail your signed proxy card in the enclosed return envelope. You may also provide your proxy instructions via phone or via the Internet by following the instructions on your proxy card or voting instruction form. Please provide your proxy instructions only once, unless you are revoking a previously delivered proxy instruction, and as soon as possible so that your shares can be voted at the Special Meeting.

If you are a shareholder of GBV, you may execute and return your written consent to GBV in accordance with the instructions provided by GBV.

| Q: | What happens if I do not return a proxy card or otherwise provide proxy instructions, as applicable? |

| A: | If you are a shareholder of Marathon, the failure to return your proxy card or otherwise provide proxy instructions will reduce the aggregate number of votes required to approve Proposal Nos. 1 and 3 and will have the same effect as voting against Proposal No. 2 and your shares will not be counted for purposes of determining whether a quorum is present at the Special Meeting. |

| Q: | May I vote in person at the Special Meeting of shareholders of Marathon? |

| A: | If your shares of Marathon’s Common Stock are registered directly in your name with Marathon’s transfer agent, you are considered to be the shareholder of record with respect to those shares, and the proxy materials and proxy card are being sent directly to you by Marathon. If you are a shareholder of Marathon of record, you may attend the Special Meeting and vote your shares in person. Even if you plan to attend the Special Meeting in person, Marathon requests that you sign and return the enclosed proxy to ensure that your shares will be represented at the Special Meeting if you become unable to attend. If your shares of Marathon’s Common Stock are held in a brokerage account or by another nominee, you are considered the beneficial owner of shares held in “street name,” and the proxy materials are being forwarded to you by your broker or other nominee together with a voting instruction card. As the beneficial owner, you are also invited to attend the Special Meeting. Because a beneficial owner is not the shareholder of record, you may not vote these shares in person at the Special Meeting unless you obtain a proxy from the broker, trustee or nominee that holds your shares, giving you the right to vote the shares at the Special Meeting. |

| 4 |

| Q: | When and where is the Special Meeting of Marathon’s shareholders? |

| A: | The Special Meeting will be held at the offices of Sichenzia Ross Ference Kesner, LLP, 1185 Avenue of the Americas, Suite 3700, New York, NY 10036 on _______, 2018. Subject to space availability, all of Marathon’s shareholders as of the record date, or their duly appointed proxies, may attend the Special Meeting. Since seating is limited, admission to the Special Meeting will be on a first-come, first-served basis. Registration and seating will begin at __________ , __________ time. |

| Q: | If my Marathon shares are held in “street name” by my broker, will my broker vote my shares for me? |

| A: | Unless your broker has discretionary authority to vote on certain matters, your broker will not be able to vote your shares of Marathon’s common stock without instructions from you. Brokers are not expected to have discretionary authority to vote for Proposal Nos. 1 or 2. To make sure that your vote is counted, you should instruct your broker to vote your shares, following the procedures provided by your broker. |

| Q: | May I change my vote after I have submitted a proxy or provided proxy instructions? |

| A: | Marathon’s shareholders of record, other than those of Marathon’s shareholders who are parties to voting agreements, may change their vote at any time before their proxy is voted at the Special Meeting in one of three ways. First, a shareholder of record of Marathon can send a written notice to the Secretary of Marathon stating that it would like to revoke its proxy. Second, a shareholder of record of Marathon can submit new proxy instructions either on a new proxy card or via the Internet. Third, a shareholder of record of Marathon can attend the Special Meeting and vote in person. Attendance alone will not revoke a proxy. If a shareholder of Marathon of record or a shareholder who owns Marathon shares in “street name” has instructed a broker to vote its shares of Marathon’s common stock, the shareholder must follow directions received from its broker to change those instructions. |

| Q: | Who is paying for this proxy solicitation? |

| A: | Marathon will pay the cost of printing and filing of this proxy statement/prospectus/information statement and the proxy card. Arrangements will also be made with brokerage firms and other custodians, nominees and fiduciaries who are record holders of Marathon’s Common Stock for the forwarding of solicitation materials to the beneficial owners of Marathon’s Common Stock. Marathon will reimburse these brokers, custodians, nominees and fiduciaries for the reasonable out-of-pocket expenses they incur in connection with the forwarding of solicitation materials. |

| Q: | Who can help answer my questions? |

| A: | If you are a shareholder of Marathon and would like additional copies, without charge, of this proxy statement/prospectus/information statement or if you have questions about the Merger, including the procedures for voting your shares, you should contact: |

Marathon Patent Group, Inc.

11601 Wilshire Blvd., Ste. 500

Los Angeles, CA 90025

(703) 232-1701

Attn: Merrick Okamoto, Chairman and Interim Chief Executive Officer

If you are a shareholder of GBV, and would like additional copies, without charge, of this proxy statement/prospectus/information statement or if you have questions about the Merger, including the procedures for voting your shares, you should contact:

Global Bit Ventures, Inc.

2 Burlington Woods Dr., Ste.100

Burlington, MA 01803

(781) 222-4347

Attn: Charles Allen, Chief Executive Officer

| 5 |

This summary highlights selected information from this proxy statement/prospectus/information statement and may not contain all of the information that is important to you. To better understand the Merger, the proposals being considered at the Special Meeting and GBV’s shareholder actions that are the subject of the written consent, you should read this entire proxy statement/prospectus/information statement carefully, including the Merger Agreement attached as Annex A, the opinion of Roth Capital Partners, LLC attached as Annex B and the other annexes to which you are referred herein. For more information, please see the section entitled “Where You Can Find More Information” in this proxy statement/prospectus/information statement.

Marathon Patent Group, Inc.

11601 Wilshire Blvd., Ste. 500

Los Angeles, CA 90025

(703) 232-1701

Marathon maintains a portfolio of patents. Marathon acquired patents and patent rights from owners or other ventures and sought to monetize the value of the patents through litigation and licensing strategies, alone or with others. On January 18, 2018, Marathon acquired four new patents related to the transmission and exchange of cryptocurrencies between buyers and sellers increasing its owned patents to 90, exclusive of patents previously contributed to a special purpose entity, which include U.S. patents and foreign patents. Marathon and certain of its subsidiaries entered into a First Amendment to Amended and Restated Revenue Sharing and Securities Purchase Agreement and Restructuring Agreement dated August 3, 2017 (the “First Amendment and Restructuring Agreement”), with DBD Credit Funding LLC (“DBD”) to restructure and replace the obligations of Marathon under an Amended and Restated Revenue Sharing and Securities Purchase Agreement, dated January 10, 2017, amending the original agreement entered into by Marathon and DBD on January 29, 2015. As contemplated in the First Amendment and Restructuring Agreement, in connection with the elimination of Marathon’s long-term debt to DBD, on October 20, 2017 Marathon entered into agreements with DBD and assigned several of its patents to a special purpose entity managed by DBD.

On October 20, 2017, we closed the First Amendment and Restructuring Agreement with DBD to restructure and replace the obligations of Marathon under that certain Amended and Restated Revenue Sharing and Securities Purchase Agreement, dated January 10, 2017, which was originally entered into on January 29, 2015. Pursuant to the First Amendment and Restructuring Agreement, certain patents were assigned to the newly created special purpose entity (“SPE”) elected by DBD, which SPE is under the management and control of an affiliate of DBD. As a result, DBD now has full, direct control over the patents under the SPE structure. Our interest of 30% of the SPE may not have any value after the recoupment of DBD ’s investment and its costs and expenses. We retain no control over, ownership of, or recourse to, the SPE’s patents. As a result, we are wholly-dependent on the efforts and experience of DBD, as well as the costs associated with the efforts of DBD, for any recoveries under these patents as to which we do not anticipate receiving any.

Global Bit Ventures, Inc.

2 Burlington Woods Dr., Ste.100

Burlington, MA 01803

(781) 222-4347

Founded in 2017, GBV is a digital asset mining company. GBV intends to power and secure the blockchain by verifying blockchain transactions using custom hardware and software. GBV intends to use its hardware to mine bitcoin (BTC) and ether (ETH), two different forms of digital assets. Bitcoin and ether rely on different technologies based on the blockchain. Wherein bitcoin is a digital currency and ether is generally associated with smart contracts and digital tokens, GBV will be compensated in digital assets by the respective blockchain network that it secures for its efforts, which is how GBV will earn revenue by mining.

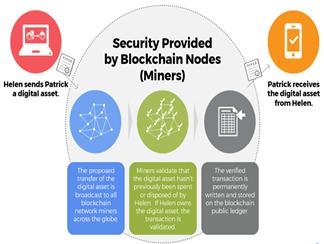

Blockchains are decentralized digital ledgers that record and enable secure peer-to-peer transactions without third party intermediaries. Blockchains enable the existence of digital assets by allowing participants to confirm transactions without the need for a central certifying authority. When a participant requests a transaction, a peer-to-peer network consisting of computers, known as nodes, validate the transaction and the user’s status using known algorithms. After the transaction is verified, it is combined with other transactions to create a new block of data for the ledger. The new block is added to the existing blockchain in a way that is permanent and unalterable, and the transaction is complete. The following illustration outlines the process of a transaction between two digital asset holders.

| 6 |

Digital assets (also known as cryptocurrency) are a medium of exchange that uses encryption techniques to control the creation of monetary units and to verify the transfer of funds. Many consumers use digital assets because it offers cheaper and faster peer-to-peer payment options without the need to provide personal details. Every single transaction made and the ownership of every single digital asset in circulation is recorded in the blockchain. Miners use powerful computers that tally the transactions to run the blockchain. These miners update each time a transaction is made and ensure the authenticity of information. The miners receive a transaction fee for their service in the form of a portion of the new digital “coins” that are issued.

| 7 |

Blockchain based transactions can involve digital assets, contracts, records, or other information.

Mining digital assets typically requires a substantial amount of specialized computer hardware and server equipment including a cost-effective data center to house the hardware. GBV has contracted with a datacenter based in Quebec, Canada, to house and run its first 1,000 specialized servers which commenced operation in late 2017.

In September 2017, GBV contracted with CIARA Technologies, a Canadian affiliate of Hypertec Group, to purchase 1,000 specialized mining servers and associated equipment for approximately $3.98 million, excluding tax. The servers are to be installed and located in Quebec, Canada at a Hypertec Group datacenter. Hypertec Systems Inc. and GBV are parties to a Master Services Agreement and GBV received initial delivery of the servers during October 2017. GBV funded the acquisition with the proceeds of the GBV Notes and other sales of its securities. GBV paid approximately $2.0 million of the purchase order during September 2017 and paid an additional approximately $1.9 8 million during November 2017. GBV currently owns 1,000 GPU mining servers with each server having 13 GPUs capable of 250 GH/s. As of the date of this proxy statement/prospectus/information statement approximately 620 servers are currently online and mining at approximately 140 GH/s in total. GBV anticipates that the remaining GPU servers will come online in February 2018 upon the completion of certain modifications being made to the data center.

In January 2018, GBV contracted to purchase 1,300 of Bitmain’s Antminer S9 miners, which are expected to utilize an estimated 1.8 MW of power once fully deployed and add 14 Ph/s of ASIC mining capacity, for a purchase price of approximately $2.6 million, excluding tax Bitmain is one of the world’s most recognized Application Specific Integrated Circuit (“ASIC”) server manufacturers. The 1,300 Antminer S9s are expected to utilize an estimated 1.8 MW of power once fully deployed and add 14 Ph/s of ASIC mining capacity. The Antminer S9s are able to mine any cryptocurrency using the SHA256 algorithm, including bitcoin. As of the date of this proxy statement/prospectus/information statement, the Antminer S9s are not online or mining.

For additional information about the aforementioned Master Services Agreement by and between GBV and Hypertec Systems, Inc., see “Reasons for Merger” on page 9.

GBV is an “emerging growth company,” as defined in Section 2(a) of the Securities Act, as modified by the Jumpstart our Business Startups Act of 2012 (the “JOBS Act”), and it may take advantage of certain exemptions from various reporting requirements that are applicable to other public companies that are not emerging growth companies including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act, reduced disclosure obligations regarding executive compensation in its periodic reports and proxy statements, and exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and shareholder approval of any golden parachute payments not previously approved.

Further, section 102(b)(1) of the JOBS Act exempts emerging growth companies from being required to comply with new or revised financial accounting standards until private companies (that is, those that have not had a Securities Act registration statement declared effective or do not have a class of securities registered under the Exchange Act) are required to comply with the new or revised financial accounting standards. The JOBS Act provides that a company can elect to opt out of the extended transition period and comply with the requirements that apply to non-emerging growth companies but any such election to opt out is irrevocable. GBV has elected not to opt out of such extended transition period which means that when a standard is issued or revised and it has different application dates for public or private companies, GBV, as an emerging growth company, can adopt the new or revised standard at the time private companies adopt the new or revised standard. This may make comparison of the GBV’s financial statements with another public company which is neither an emerging growth company nor an emerging growth company which has opted out of using the extended transition period difficult or impossible because of the potential differences in accountant standards used.

Global Bit Acquisition Sub, Inc.

Merger Sub is a wholly owned subsidiary of Marathon, and was formed solely for the purposes of carrying out the Merger.

If the Merger is completed, Merger Sub will merge with and into GBV, with GBV surviving as a wholly owned subsidiary of Marathon.

At the Effective Time of the Merger, each share of (A) GBV Common Stock will automatically be cancelled and converted into shares of either Marathon’s Series C Preferred Stock or Marathon’s Common Stock: (B) GBV Series A Stock will automatically be cancelled and converted into shares of either Marathon’s Series C Preferred Stock or Marathon’s Common Stock; and (C) all of GBV Notes will automatically be cancelled and converted into shares of either Marathon’s Series C Preferred Stock or Marathon’s Common Stock. Marathon will not assume outstanding and unexercised warrants and options to purchase shares of GBV’s capital stock, and none are outstanding. The total number of shares of Marathon’s Common Stock and Common Stock that is issuable under the Series C Preferred Stock is 126,674,557. After the completion of the Merger, Marathon will change its corporate name to “Marathon Blockchain, Inc.” or similar name determined by the board of directors of Marathon as required by the Merger Agreement.

| 8 |

The closing of the Merger will occur no later than the second business day after the last of the conditions to the Merger has been satisfied or waived (other than those conditions that by their nature are to be satisfied at the closing, but subject to the satisfaction or waiver of each such conditions), or at such other time as Marathon and GBV agree. Marathon and GBV anticipate that the consummation of the Merger will occur in the first quarter of 2018. However, because the Merger is subject to a number of conditions, neither Marathon nor GBV can predict exactly when the closing will occur, or if it will occur at all.

Although each of GBV and Marathon have invested in additional servers and acquired additional assets since the execution of the Merger Agreement, the parties have agreed that the Merger Consideration (as defined herein) will not be adjusted as a result of such purchases.

Reasons for the Merger (see page 67)

In connection with Marathon’s agreement to acquire GBV, Marathon has secured financing in connection with winding down the patenting business and working capital for reduced operations while it prepares for the acquisition of GBV. Marathon is transitioning from its historic business into businesses involved in supporting the blockchain and digital asset (cryptocurrency) ecosystem , although Marathon may continue to acquire intellectual property related to and seek to enforce patents involving blockchain and digital asset technologies directly or with third parties. While reducing its reliance on patent enforcement and licensing for the generation of revenue, Marathon has undertaken steps to dedicate its resources and efforts towards blockchain and digital asset (cryptocurrency) acquisition. Cryptocurrencies are one form of digital assets. As a result, we sometimes use the phrases “cryptocurrency” and “digital assets” interchangeably. These activities include the acquisition of businesses and assets engaged in or necessary for supporting the business of mining, as described below, including the direct acquisition of businesses, equipment and technology that service the blockchain ecosystem as well as the outright acquisition of digital assets, such as cryptocurrency, that may be held for appreciation or exchanged for other digital or non-digital assets or sold. Marathon intends to complete the acquisition of GBV and enter into a new and unproven business model with significant risks, both known and unknown, as more fully described in the section titled “Risk Factors”, below. In connection with that newly-adopted business strategy, Marathon anticipates it will be necessary to add personnel to the management team, as well as other personnel, to enhance assessment of controls over risks, to review and seek approval of regulatory bodies (including the NASDAQ Capital Market for continued listing of its Common Stock) and will face other uncertainties associated with the evolving business and regulatory risks of blockchain and digital assets (cryptocurrency). There is no assurance that Marathon will be able to successfully navigate these risks or that regulatory and other requirements will not have a material adverse effect on the goals and objectives of Marathon or prevent Marathon from realizing its objectives.

On September 27, 2017, GBV placed a purchase order with Ciara Technologies, Inc., a company incorporated under the laws of Canada (“Ciara”), whereby Ciara agreed to sell certain equipment to GBV pursuant to a Master Services Agreement (the “Master Services Agreement”) dated December 15, 2017, with Hypertec Systems, Inc., a company incorporated under the laws of Canada which is an affiliate of Ciara (“Hypertec Systems”). In accordance with the terms and subject to the conditions of the Master Services Agreement, Hypertec Systems, or its affiliates, agents, suppliers or subcontractors, shall provide to GBV, the services and equipment which are set forth in the Master Services Agreement, including the equipment in the purchase order, for a term of 36 months (the “Term”), which term is automatically renewable for additional one year periods unless GBV gives notice of termination. Pursuant to the Master Services Agreement, Hyertec Systems shall provide such standard services as may be requested by GBV from time to time, including, but not limited to (i) providing dedicated floor space for equipment and storage, (ii) heating, ventilation, air conditioning and fire suppression facilities, (iii) sufficient electrical power, (iv) multiple security level including turnstile doors, access codes and biometrics, (v) on-site staff 24-hours/7-days, (vi) access to one CAT5E for internet connectivity and (vii) access to one steel shelf for every 25kW of power required (the “Services”). In exchange for such Services during the Term, GBV shall pay to Hypertec Systems a monthly recurring charge for base capacity reservation fees (“MRC”), and any applicable charges including, but not limited to, features and installation charges. Hypertec Systems shall provide all services, free of charge, except for Managed Internet Bandwidth Services, dedicated secured storage spare and the kWh used, until such time as the servers purchased from Ciara are running at a hash rate of at least two hundred and thirteen (213) gigahash per second for a period of five (5) consecutive days as determined by Hypertec Systems , provided that it is consistent with the hash rate shown on GBV’s pool. The equipment purchased from Ciara pursuant to the purchase order dated September 27, 2017, had a purchase price of approximately $3.98 million, excluding tax, and consisted of mining servers and other related equipment. In addition to the MRC, GBV shall also reimburse Hypertec Systems for actual metered power used by GBV at the actual kWh rates paid by Hypertec Systems to its power provider, on a monthly basis, multiplied by the power usage effectiveness. GBV has the ability to request other optional services from Hypertec Systems for additional costs. Hypertec Systems is required to maintain certain insurance levels covering the equipment of GBV, which equipment is housed on their premises. In connection with GBV’s purchase of 1,300 additional Antminer S9 miners, these servers have not been installed, and GBV is currently seeking an appropriate location to install these servers.

Following the Merger, the combined organization will focus on the development of GBV’s new business involving the blockchain ecosystem and generation of digital assets. GBV is focused on mining digital assets and intends to add specialized computer equipment and plans to expand its activities to mine new digital assets.

| ● | Management Team. It is expected that the combined organization will be led by the management from GBV and a board of directors with representation from each of Marathon and GBV. | |

| ● | Cash Resources. The combined organization is expected to have approximately $8.0 million in cash and cash equivalents at the closing of the Merger, which Marathon and GBV believe is sufficient to enable GBV to implement its near-term business plans. |

| 9 |

Opinion of the Marathon Financial Advisor (see page 67)

A written opinion dated December 13, 2017, addressed to Marathon’s board of directors, provided a “fairness opinion” to the effect that, as of the date of the opinion and based on and subject to various assumptions, qualifications and limitations described in the opinion, the aggregate consideration to be paid by Marathon in the proposed Merger was fair, from a financial point of view, to holders of Marathon’s Common Stock. Roth Capital Partners, LLC (“Roth”) rendered the opinion. The full text of this written opinion to Marathon’s board of directors, which describes, among other things, the assumptions made, procedures followed, factors considered and limitations on the review undertaken, is attached as Annex B to this proxy statement/prospectus/information statement and is incorporated by reference in its entirety herein. Holders of Marathon’s Common Stock are encouraged to read the opinion carefully in its entirety.

The opinion was provided to Marathon’s board of directors in connection with its evaluation of the aggregate consideration to be paid for by Marathon in the Merger. It does not address any other aspect of the proposed Merger or any alternative to the Merger and does not constitute a recommendation as to how Marathon’s shareholders of Marathon should vote or act in connection with the Merger or otherwise.

| 10 |

Overview of the Merger Agreement

Merger Consideration (see page 76)

At the Effective Time, all outstanding shares of GBV ’s capital stock and GBV Notes shall convert into the right to receive shares of Marathon’s Series C Preferred Stock or Common Stock as follows:

| ● | At the Effective Time of the Merger, each share of (A) common stock of GBV, par value $0.0001 per share (“GBV Common Stock”) will automatically be cancelled and converted into shares of either (x) Series C Preferred Stock of Marathon (the “Series C Preferred Stock”) or (y) common stock, par value $0.0001 per share of Marathon (“Common Stock”): (B) Series A Preferred Stock, par value $0.0001 per share, of GBV (“GBV Series A Stock”) will automatically be cancelled and converted into shares of either (x) Series C Preferred Stock or (y) Common Stock; and (C) all of GBV’s outstanding convertible debt (“GBV Notes”) will automatically be cancelled and converted into shares of either Marathon’s Series C Preferred Stock or Common Stock. Marathon will not assume outstanding and unexercised warrants and options to purchase shares of GBV’s capital stock, and none are outstanding. The total number of shares of Marathon’s Common Stock and Common Stock that is issuable under the Series C Preferred Stock is 126,674,557. | |

| ● | Marathon shareholders will continue to own and hold their existing shares of Marathon’s Common Stock and Marathon’s preferred stock. Marathon debt holders owning $ 2,613,948 of 5% convertible promissory notes (the “Marathon Notes”) as of January 22, 2018 , will convert their unconverted notes into Series E-1 Convertible Preferred Stock of Marathon (“Series E-1 Preferred Stock”) if not converted to Common Stock prior to the Merger. Marathon Series E Convertible Preferred Stock (“Series E Preferred Stock”) holders owning 5, 511.70 shares of Series E Preferred Stock convertible into 5, 511,702 shares of Common Stock) as of January 22, 2018 will continue to remain outstanding. The vesting of 448,775 unexercised options to purchase shares of Marathon’s Common Stock, which are substantially vested, will remain outstanding as of the closing of the Merger. All 794,717 warrants to purchase shares of Marathon’s Common Stock are currently exercisable into 794,717 shares of Common Stock. The Marathon’s Common Stock, preferred stock, warrants and options will remain in effect pursuant to their terms. Immediately after the conversion of the GBV Common Stock, the GBV Series A Stock and the GBV Notes, Marathon shall have issued 81% of its issued and outstanding Common Stock, on a fully-diluted basis, under the Merger Agreement to GBV prior to giving effect of the issuance of 1 million shares of Marathon’s Common Stock on December 13, 2017 at $5.00 per share in a registered offering subsequent to the Merger Agreement and other changes in Marathon’s capitalization following the date of the Merger Agreement. For these purposes, Marathon’s fully-diluted Common Stock is defined as the outstanding common stock of Marathon, plus conversion of preferred stock, options and warrants of Marathon, prior to the registered offering (the “Fully-Diluted Common Stock of Marathon”), with Marathon current shareholders, the holders of the Marathon Notes, option holders and warrant holders owning, or holding rights to acquire, approximately 19% the Fully-Diluted Common Stock of Marathon upon closing of the Merger (as such percentages are increased or reduced for the registered offering and any other shares issued or cancelled prior to the closing of the Merger). |

| ● | After the completion of the Merger, Marathon will change its corporate name to “Marathon Blockchain, Inc.” or similar name determined by the board of directors of Marathon as required by the Merger Agreement. For a more complete description of the Merger exchange ratio please see the section entitled “The Merger Agreement” in this proxy statement/prospectus/information statement. |

The Merger Agreement does not include a price-based termination right, and there will be no adjustment to the total number of shares of Marathon’s Common Stock that GBV’s shareholders will be entitled to receive for changes in the market price of Marathon’s Common Stock after the date the Merger Agreement was signed. Accordingly, the market value of the shares of Marathon’s Common Stock issued pursuant to the Merger will depend on the market value of the shares of Marathon’s Common Stock at the time the Merger closes, and could vary significantly from the market value on the date of this proxy statement/prospectus/information statement and the date of the Merger Agreement. The full text of the Merger Agreement is incorporated by reference into this proxy statement/prospectus/information statement.

| 11 |

Treatment of Marathon’s Stock Options and Warrants (see page 135)

The number of shares of Marathon’s Common Stock underlying such options and the exercise price for such options as of January 22, 2018, is 448,775, which are substantially vested, at a weighted average exercise price of $16.22. The terms governing options to purchase Marathon’s Common Stock will otherwise remain in full force and effect following the closing of the Merger.

On November 28, 2017, Marathon entered into an exchange agreement with the holders of outstanding warrants to purchase 6,656,000 shares of the Marathon’s Common Stock, originally issued on August 31, 2017 and on September 27, 2017, and such holders exchanged such warrants and relinquished any and all rights thereunder for 5,511.70 shares of Marathon’s newly authorized Series E Preferred Stock, based on the cashless exercise calculation of the warrant. The 5,511.70 shares of Series E Preferred Stock, issued on November 30, 2017, are convertible into an aggregate of 5,511,702 shares of Common Stock.

The Series E Preferred Stock is convertible into shares of Common Stock based on a conversion calculation equal to the stated value of each share of Series E Preferred Stock, plus all accrued and unpaid dividends, if any as of such date of determination, divided by the conversion price. The stated value of each share of Series E Preferred Stock is $6,000 and the initial conversion price is $6.00 per share, subject to adjustment for stock splits, stock dividends, recapitalizations, combinations, subdivisions or other similar events. The Series E Preferred stock, with respect to dividend rights and rights on liquidation, winding-up and dissolution, in each case will rank senior to Marathon’s Common Stock and all other securities that do not expressly provide that such securities rank on parity with or senior to the Series E Preferred Stock. Until converted, each holder of Series E Preferred Stock shall be entitled to the number of votes equal to the number of shares of Common Stock such Series E Preferred Stock is convertible into (voting as a class with Common Stock), but not in excess of the conversion limitations set forth in the Certificate of Designation of Rights, Powers, Preferences, Privileges and Restrictions of the 0% Series E Convertible Preferred Stock (the “Series E Certificate of Designation”).

Without limiting any other provision of the Series E Certificate of Designation, Marathon may not authorize or issue any additional or other shares of capital stock that is (i) of senior rank to the Series E Preferred Stock in respect of the preferences as to dividends, distributions and payments upon the liquidation, dissolution and winding-up of Marathon, (ii) of pari passu rank to the Series E Preferred Stock in respect of the preferences as to dividends, distributions and payments upon the liquidation, dissolution and winding-up of Marathon or (iii) any junior stock having a maturity date (or any other date requiring redemption or repayment of such shares of such junior stock) that is prior to the date on which any Series E Preferred Stock shall remain outstanding, without the prior express consent of the holders of at least a majority of the outstanding shares of Series E Preferred Stock, voting separate as a single class.

The Series E-1 Preferred Stock issued pursuant to the Merger Agreement will rank junior in all respects to the Series E Preferred Stock.

Treatment of GBV’s Stock Options and Warrants (see page 75)

There are no options, warrants, rights, convertible or exchangeable securities, “phantom” stock rights, stock appreciation rights, stock-based performance units, commitments, contracts, arrangements or undertakings of any kind to which GBV is a party or by which GBV is bound (i) obligating GBV to issue, deliver or sell, or cause to be issued, delivered or sold, equity interests in, or any security convertible or exercisable for or exchangeable into any equity interest in, GBV, (ii) obligating GBV to issue, grant, extend or enter into any such option, warrant, call, right, security, commitment, contract, arrangement or undertaking or (iii) that give any person the right to receive any economic benefit or right similar to or derived from the economic benefits and rights occurring to holders of GBV Common Stock.

Conditions to the Completion of the Merger (see page 135)

To consummate the Merger, Marathon’s shareholders must approve (a) the Merger Agreement and the transactions contemplated thereby, including the Merger and the issuance of shares of Marathon’s Common Stock in the Merger, and (b) an amendment to the Amended and Restated Articles of Incorporation of Marathon effecting the Marathon Name Change. Additionally, GBV’s shareholders must adopt the Merger Agreement thereby approving the Merger and the other transactions contemplated by the Merger Agreement. In addition to obtaining such shareholder approvals and appropriate regulatory approvals, each of the other closing conditions set forth in the Merger Agreement must be satisfied or waived.

No Solicitation (see page 140)

Subject to any fiduciary obligations applicable to its boards of directors, under the Merger Agreement Marathon and GBV shall not (and shall not cause or permit any of their affiliates to) engage in any discussions or negotiations with any person or take any action that would be inconsistent with the transactions contemplated by the Merger Agreement. GBV shall notify Marathon immediately if any person makes any proposal, offer, inquiry, or contact with respect to any of the foregoing. Marathon shall notify GBV immediately if any person makes any proposal, offer, inquiry or contact with respect to any of the foregoing.

Marathon and GBV also agree they will consult with each other before issuing, and provide each other the opportunity to review and comment upon, any press releases or other public statements with respect to the Merger Agreement or the Merger and shall not issue any such press release or make any such public statement prior to such consultation, except as may be required by applicable law, court process or by obligations pursuant to any listing agreement with any national securities exchanges.

Termination of the Merger Agreement (see page 145)

Either Marathon or GBV can terminate the Merger Agreement under certain circumstances, which would prevent the Merger from being consummated. The Merger Agreement provides for closing of the Merger on or before February 28, 2018, as the “outside termination date”. However, Marathon and GBV intend to amend the Merger Agreement to extend the termination date to March 15, 2018, subject to consecutive 14-day extensions upon mutual written consent, but no later than April 30, 2018. Any further extensions after April 30, 2018, shall require a mutual agreement between Marathon and GBV.

| 12 |

Termination Fee (see page 147)

Neither Marathon nor GBV will be required to pay any termination fees or reimburse the other party for expenses incurred in connection with the Merger.

In September 2017, GBV issued aggregate amount of $2,000,000 in secured convertible notes payable, or the GBV Notes, to multiple investors. The GBV Notes are convertible into GBV’s common stock at $0.20 per share, subject to adjustments including an adjustment upon issuance of subsequent shares of common stock, have a 5% annual interest rate and mature on March 6, 2019 and March 28, 2019. The GBV Notes are secured by all assets and properties of the Company. On October 17, 2017, GBV issued a secured convertible note to an investor for $1,750,000 convertible into GBV Common Stock at $0.20 per share, subject to adjustments including an adjustment upon issuance of subsequent shares of common stock, has a 5% annual interest rate and matures on March 28, 2019. The GBV Notes will be converted into Marathon’s Series C Preferred Stock or Common Stock at the Effective Time of the Merger.

Certain current shareholders and holders of the Marathon Note own GBV Notes in addition to their Marathon holdings and will receive additional shares of Marathon’s Series C Preferred Stock or Common Stock upon the closing of the Merger.

It is expected by both Marathon and GBV that all of Marathon’s shareholders and holders of the Marathon Note who are GBV shareholders or holders of the GBV Notes will cast all of their votes for approval of Proposal Nos. 1 and 2.

Support and Voting Agreements (see page 74)

On November 1, 2017, Marathon entered into an amendment with Doug Croxall, Marathon’s Chief Executive Officer (the “Amendment to Retention Agreement”), to amend the retention agreement signed on August 22, 2017 , whereby his tenure as Chief Executive Officer would be extended until December 31, 2017. Mr. Croxall entered into a Voting and Standstill Agreement on November 1, 2017, whereby he agreed to vote all of the shares he either directly or beneficially owns or acquires as instructed by Marathon’s board of directors and to not sell any shares until 10 days after a change of control as defined in the agreement. Mr. Croxall received 700,000 shares of Marathon’s Common Stock in connection with the agreements.

Lock-Up Agreements (see page 74)

As of January 22, 2018, Marathon’s shareholders who have committed to execute lock-up agreements beneficially owned in the aggregate approximately 5.9% of the outstanding shares of Marathon’s Common Stock.

| 13 |

Management Following the Merger (see page 78 )

The Merger Agreement does not specify or require specific management appointments. Marathon and GBV are expected to agree to a management team to afford continuity to the combined companies as well as management with skills in blockchain and digital assets businesses. It is expected that the appointment of all management and directors will be determined prior to the closing of the Merger.

Interests of Certain Directors, Officers and Affiliates of Marathon and GBV (see pages 76 and 90 )

In considering the recommendation of Marathon’s board of directors with respect to the issuance of Marathon’s Common Stock pursuant to the Merger Agreement and the other matters to be acted upon by Marathon’s shareholders at the Special Meeting, Marathon’s shareholders should be aware that certain members of Marathon’s board of directors and executive officers of Marathon have interests in the Merger that may be different from, or in addition to, interests they have as Marathon’s shareholders. For example, Marathon has entered into certain agreements with each of its remaining executive officers (Doug Croxall and Francis Knuettel II) that may result in the receipt by such executive officers of cash severance payments and other following the Effective Time of the Merger, and have received cash payments and other benefits in connection with the Merger Agreement prior to the Effective Time (collectively, not individually, and excluding the value of any accelerated vesting of equity awards).

| 14 |

Doug Croxall, Marathon’s Chief Executive Officer, will receive a retention payment in the total amount of $500,000 pursuant to the Amendment to Retention Agreement, of which payment $312,500 was paid previously and $187,500 is payable upon the closing of the Merger.

As of January 22, 2018 , Marathon’s directors and executive officers beneficially owned, in the aggregate approximately 7.6 % of the outstanding shares of Marathon’s Common Stock which will be shares of the parent company of GBV following the Merger.

In considering the recommendation of GBV’s board of directors with respect to approving the Merger and related transactions by written consent, GBV’s shareholders should be aware that certain members of GBV’s board of directors and certain of GBV’s executive officers have interests in the Merger that may be different from, or in addition to, interests they have as GBV’s shareholders. For example, certain of GBV’s directors and executive officers or their family members have invested in the GBV Notes and acquired “founders” shares at reduced prices than may have been available to other GBV shareholders but which will be exchanged, at the closing of the Merger, and become shares of Marathon’s Series C Preferred Stock or Common Stock at the same ratio of other GBV Common Stock, GBV Series A Stock and GBV Notes, certain of GBV’s directors and executive officers are expected to become directors and executive officers of Marathon upon the closing of the Merger, and all of GBV’s directors and executive officers will be entitled to certain indemnification and liability insurance coverage pursuant to the terms of the Merger Agreement or upon closing of the Merger.

As of January 22, 2018 , all of GBV’s directors and executive officers, together with their affiliates, owned approximately 3. 5 % of the outstanding shares of GBV’s capital stock, on an as converted to common stock basis.

Both Marathon and GBV are subject to various risks associated with their businesses and their industries. In addition, the Merger poses a number of risks to each company and its respective shareholders, including the possibility that the Merger may not be completed and the following risks:

| ● | The exchange share issuance amounts under the Merger Agreement are not adjustable based on the market price of Marathon’s Common Stock, so the Merger consideration at the closing may have a greater or lesser value than at the time the Merger Agreement was signed. For example on December 11, 2017, Marathon closed on a sale of one million shares with a $5 million investment in its Common Stock and of 1,354,546 shares with a $7.4 million investment in its Common Stock , as a result of which the Merger Agreement was amended to provide for removal of a percentage ratio and only the share issuance amounts will be issued as agreed; | |

| ● | The exchange share issuance amounts under the Merger Agreement are not adjustable based on the net cash of either Marathon or GBV at the Effective Time, so the relative ownership of the combined organization as between current shareholders of GBV and current shareholders of Marathon may not reflect the ratio of net cash of Marathon and GBV, respectively, at the closing of the Merger; | |

| ● | The Merger may be completed even though material adverse changes may result solely from the announcement of the Merger, changes in the industry in which Marathon and GBV operate that apply to all companies generally and other causes; | |

| ● | Some of Marathon’s and GBV’s respective officers and directors have interests that are different from or in addition to those considered by other shareholders of GBV and Marathon and which may influence them to support or approve the Merger; | |

| ● | The market price of the combined organization’s (Marathon’s) common stock may decline as a result of the Merger; | |

| ● | Marathon’s and GBV’s shareholders may not realize a benefit from the Merger commensurate with the ownership dilution they will experience in connection with the Merger; | |

| ● | During the pendency of the Merger, Marathon and GBV may not be able to enter into a business combination with another party under certain circumstances because of restrictions in the Merger Agreement, which could adversely affect their respective businesses; |

| 15 |

| ● | Certain provisions of the Merger Agreement may discourage third parties from submitting alternative takeover proposals, including proposals that may be superior to the arrangements contemplated by the Merger Agreement; | |